NEO Finance - what are the real returns?

Some investors were surprised about “C“ rating assigned to NEO Finance in my platform ratings for February 2020. And of course, the team behind NEO Finance was not happy as well:

So let me explain, why I gave this platform only a “C“ rating, which in my description means following: “Overpromise, underdeliver. Misleading claims, very high risk & unproportionally low yield. Bad risk/reward ratio“.

1000 EUR test

I did a test with 1000 EUR investment in NEO Finance from March 2019 till August 2019. When I started, in NEO website there was a promise - that average returns for investors are 14%, now they say - it is 12%. So let’s see what were the actual returns that I could achieve?

Auto Invest - attempt #1

At the start I wanted to set up an Auto Invest portfolio, invest in loans with term 12 months or less, and have a “buyback guarantee“. NEO Finance has a bit different approach than other platforms - there is no buyback guarantee, but instead you can use their “Provision Fund“ - pay a fee, and then if a loan fails, your principal will be paid back - so you won't make any profit, but also won't have losses.

But there were 3 problems:

When creating Auto Invest portfolio, I could not see - how many loans would match my criteria

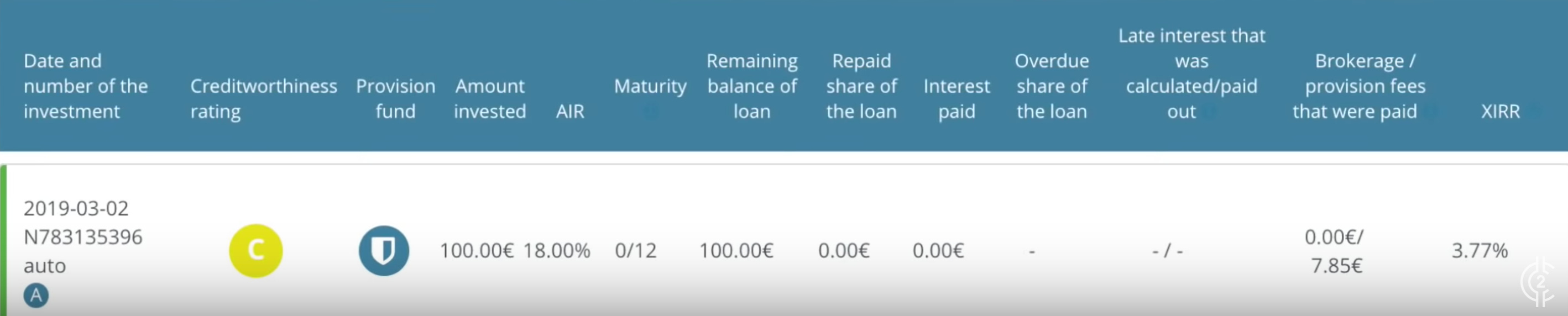

After activating portfolio - it turned out, that there were not enough loans and I had to wait for some time to get even 1 active investment

The real return for my first 100 EUR investment from this portfolio was completely different than what I expected. It was only 3.77%:

Auto Invest - attempt #2

I was unpleasantly surprised that from one side - in all website the things that are advertised and stats shown etc., are these interest rates that borrowers pay, but they are not really a useful indicator to an investor about his expected returns.

There is no way for an investor to predict - what will be his real return based on NEO Finance loan ratings, terms or any other parameters. So the only option is to invest and hope, that the return will be as good as promised on homepage.

To get some kind of sense of real returns, I set up an Auto Invest portfolio that would invest max 10 EUR in one loan, and I selected all ratings: A, B, C and also all the range of interest rates, and all possible terms: from 3 to 60 months. And I also enabled the “Provision fund“:

In next 2 weeks 11 more investments were made from this portfolio, and the XIRR numbers were not better than in my first 100 EUR investment. The real return ranged from 0% to 4.57%, average from all of them: 3.22%

Auto Invest - attempt #3

I thought - ok, this is bullshit. Why would I invest in a P2P platform to get 3.2% return, if I can go to 10 other platforms and get 3x higher return without such a hassle? Maybe for someone 3.2% return is fine from a P2P platform, but I see that as a very bad risk/reward ratio.

But I wanted to give this platform another chance and check, if I would invest in loans without this “Provision Fund” enabled, maybe then the returns would become somewhere closer to their promises? I still had 800 EUR to invest, so I set up another Auto Invest portfolio - max 40 EUR in 1 loan, all ratings, from 14% and with term: from 3 to 12 months, without Provision fund enabled:

My initial plan was to get this money invested and then after 9-12 months check - how many of loans are late, how many - returned, and what is the real return.

But in the next months the investing happened very slowly and I managed to invest only 12 * 40 = 480 EUR, so a big part of money was uninvested, and taking into account all the other stuff I lost patience and sold everything, and withdraw all money.

From these 12 loans 2 were repaid and they had a very high 16.5% return:

But in others it was complete random, from -16% up to +12% return:

Final results

My expectations: from 1000 EUR in 5 months with 12% return I should have earned about 50 EUR. What was the reality?

+ €20.09 interest earned

- €3.34 deducted for tax payments

- €21.51 paid in different fees

So in total after 5 months of “investing“ I lost €2.76, which would mean -0.66% return per year.

Note that I also received a €20 sign up bonus and was paid €300 to do the platform review on my YouTube channel, so in the end I cannot really complain about losing money, but I don't plan to use this platform anymore and cannot recommend it to anyone else.

What I like about NEO Finance?

Each investor has his own IBAN account

Good on-boarding process and support

NEO Finance has EMI licence - client money is kept in an account separate from that of the company. Company is supervised by the Bank of Lithuania.

What I hate about NEO Finance?

Very few loans with term 3-12 months, cannot invest even 1000 EUR

Over complicated “Provision fund“

No way to predict returns before investing

Real returns are much lower than expected and advertised

Website and platform has lot of content and functionality that is not important, and gives an impression it is created to distract investors, while at the same time - key things are missing

Many fees that again over complicate the investing process and can drive down the real return below 0%

What could NEO Finance improve?

Remove “Provision fund“ with it’s complicated fee structure, all consumer loans should have a “Buyback guarantee“ - it is NEO Finance’s job to decide, to whom give out a loan and predict - how likely the loan will be given back. A retail investor has no skills and no data to make an informed decision about this, so he/she should not take these decisions or take the risk associated with that.

Remove all the useless crap from Auto Invest: “additional criteria“ and loan ratings, instead - provide buyback guarantee and estimate - how many loans are available straight away + in next 30 days, based on loan term selected (+ interest, if it varies for different terms).

Stop misleading investors by advertising 17.29% “average interest rate“ - which most investors would expect to be their return, but in reality - turns out that is the interest borrowers pay, and has no connection to the return that investors will get. Maybe take an example from Viainvest and offer fixed return for all consumer loans.

Good example: Viainvest - in their stats page shows 11% “average interest rate”. And guess what - investors actually get paid 11% return for their investments. Easy, right?

Bad example: NEO Finance - in their stats page show 17.29% “average interest rate“. But my return for loans with “provision fund“ enabled was 3.2%. WTF?

Key takeaways

NEO Finance seems to be very solid when it comes to platform security, it even did an IPO and you can trade it’s stock

Real returns are much lower than promised, with “Provision fund“ enabled: 3.22%

Not possible to predict returns before making investment

Whole website and platform confuses investor, investing is too complicated

Risk/reward ratio is bad, NEO Finance offers 2 bad options:

a) getting 3.22% with Provision Fund enabled, too low return from a P2P platform

b) risking all investment without any idea about end result - does not make sense

Update on 18.02.2020

Here is a comment from NEO Finance:

On behalf of NEO Finance team I will try to explain why your results in NEO Finance are different from your initial expectation.

As there are many investors, there are also many investment strategies. However, in NEO Finance platform there are three main strategies.

1. Investing with a Provision Fund. Provision Fund is created for a very conservative investor whose primary goal is to secure principle and then seek for profit. Provision Fund allows investors to reduce their investment risk: if a loan defaults, NEO Finance guarantees to repay all remaining principle to investors. Provision Fund guarantees that you won't have any loss before tax. So, in the result, low risk = Low reward.

2. Holding investment true the all maturity period. And if the loans become defaulted, hold untill the debt recovery recovers principle and interest. (Page 13th) https://www.paskoluklubas.lt/.../Sales%20report%202019Q4.... This strategy asks for at least 3 years of consistent investment because investment results depend on successful recovery in the long term.

3. BuyBack (Yes, we do have it since 2017). When agreements with borrowers are terminated, investors can sell their defaulted investments for 50-80% of their face value to NEO Finance.

NEO Finance is not issuing payday loans but instead issuing consumer loans for borrowers, sometimes in even better conditions than a commercial bank could offer. In this case, the borrowers prefer a longer period of loan repayment (average loan term is 48 months). So there aren’t many short-term offers for investors. NEO Finance sees investing as a long-term action.

Ever since your last investment activities, the platform has been constantly improving. For example, now you are able to see your Auto investment efficiencies.

How to predict a profit in NEO Finance? In the majority of regulated investment assets there is always uncertainty regarding potential profit predictions. Your profit will always be LOWER than the interest rates due to default occurrence and annuity schedule. Also, profit will be varied by the creditworthiness rating and strategies you choose. You can never expect the same performance from different creditworthiness ratings. https://www.neofinance.com/en/statistics

Summarizing what have led you to such results:

*Conservative strategy at the beginning with a Provision Fund. Low risk = low reward.

*Selling your investment with a discount into the secondary market before the end of the maturity period.

So how to achieve average return rate of 12% in NEO Finance? If we rely on historical data and assume that market conditions would not change in the near future:

* Have a strategy.

* Take an extra risk in order to get potentially better results (Investing with or without BuyBack and invest without Provision Fund).

* Wait untill the end of the maturity.

*Re-invest and diversify your remaining balance.

* Do not let the panic and emotions to control you and your investment.

And I talked to some other NEO Finance investors - their returns ranged from negative to the advertised average of 12%. For me the unpredictability is enough to stay away, but for those - who want to test NEO Finance themselves, the best strategy to NOT lose money and make higher return than in my examples could be following:

If you don't like gambling, enable Provision Fund

Avoid C loans - too high fees for Provision Fund, many of loans are repaid back early or are not paid in time and the “Provision Fund“ gets triggered - which means 0% return

Avoid short-term loans, choose the term: 24 months or longer. It takes time to “pay“ for Provision fund fees.

Look out for cash drag - if your Auto Invest settings are too strict, it might take time to invest money.

And here is an example from Auto Invest settings that produced about 11% return. According to investor who set up these portfolios, interest rates in NEO Finance dropped last year and now investors could expect about 2% lower return:

Want to get access to exclusive content? Become a paid subscriber:

Or join “High-risk investments“ Telegram group for an informal discussion.