Mintos & conflicts of interest, Part 2

The first part of this blog post was focused on past events, but in second part I will discuss possible future events.

What is Funderly Group?

When I first noticed it, I thought it was created for a new loan originator, but Mogo CFO corrected me and informed that AS “Funderly Group” was created by Mogo for acquiring Sebo. Timeline:

12.05.2020: AS Funderly Group is created, registered capital: 500 000 EUR

06.07.2020: AS Funderly Group registered capital is increased to: 4 000 000 EUR

13.07.2020: Mogo & Sebo deal announced to Mintos investors

15.07.2020: Mogo & Sebo deal announced to Mogo bond holders

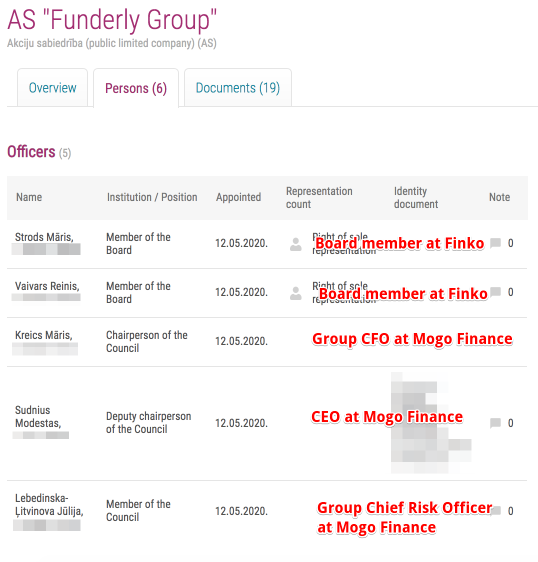

If we look at “persons“ section of AS Funderly Group, we see 2 Finko board members and 3 persons from Mogo: CFO, CEO, Chief Risk Officer

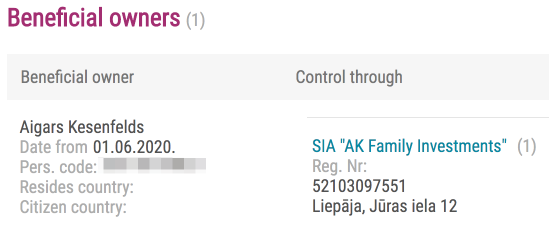

And as usual, the only beneficial owner is Aigars Kesenfelds:

The interesting thing to note - it took 2 months from creating this holding company until the announcement of a deal between Mogo and Finko.

More similar deals in progress?

Not everyone is aware, but there is quite a big list of loan originators on Mintos that are in some way related to Mintos shareholders. In most cases there is shareholder overlap, in some cases (DelfinGroup) there were pledges between legal entities, where the beneficial owner of pledgee is one of Mintos shareholders.

Another thing in common - most of them have headquarters in Skanstes iela 52:

So I looked up what other companies were recently set up in Skanstes iela 52, and some interesting stuff came up:

01.06.2020: AS "YC Group", registered capital: 2 000 000 EUR

19.06.2020: AS "Zen Group", registered capital: 35 000 EUR

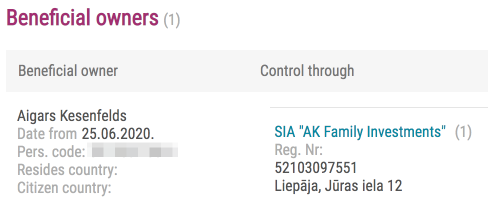

25.06.2020: AS "NF Capital", registered capital: 35 000 EUR

02.09.2020: AS "NF Capital", capital increased to: 1 500 000 EUR

AS “YC Group“

Just like in Sebo case, we see the same 3 persons from Mogo: CFO, CEO and Group Chief Risk Officer.

And of course, the only beneficial owner is Aigars:

Una Hevita - according to her LinkedIn profile, from Dec 2018 to Nov 2019 she was COO at Cash On Go Ltd. = Peachy, the loan originator that announced wind-down on 06.03.2020. According to company register, Una is officer at SIA FT Ventures, Member of the Board at SIA EC Finance Group (part of AS Puzzle Investments), beneficial owner of AS "ExpressCredit Holding".

Girts Suberts - according to LinkedIn, Girts is Board Member at Orange Sky Finance and board member at ExpressCredit.co.zm, according to company register, Girts is member of board at SIA "EC Finance Group" (part of AS Puzzle Investments) and member of board at AS "ExpressCredit Holding".

Edgars Sprogis - according to LinkedIn, Edgars is CFO at Orange Sky Finance.

Orange Sky Finance = Expresscredit?

From LinkedIn descriptions:

Orange Sky Finance is a global consumer finance company. With a shared service centre and regional head offices in Latvia and Mauritius, Orange Sky Finance operates across 5 markets in Sub-Saharan Africa.

ExpressCredit is a global consumer finance fintech operating in Sub-Saharan region

In short - I see a past connection to Peachy and current connection to ExpressCredit:

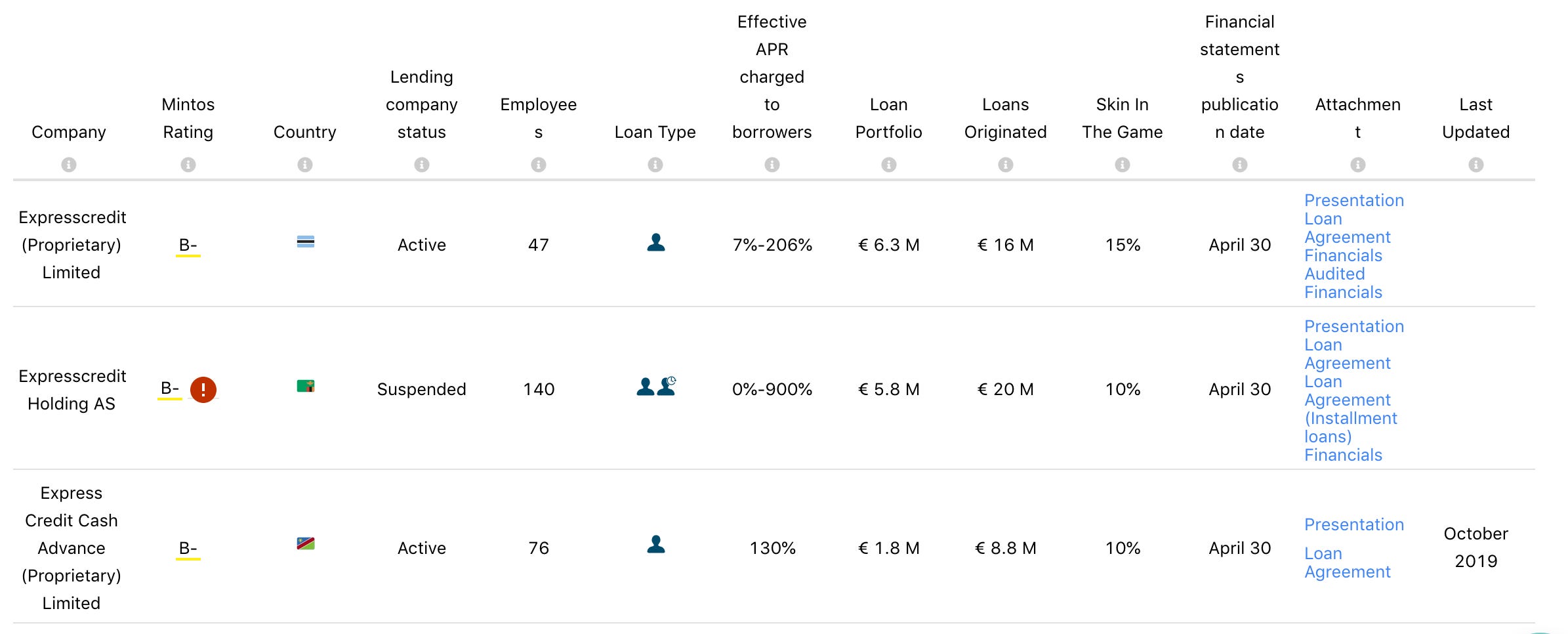

Just like in Finko and Finitera, we can see that one of Expresscredit companies is having issues - Expresscredit Holding AS that operates in Zambia, is suspended. Outstanding loans: 3 316 063 EUR.

Just for fun, let’s quote what ExpressCredit wrote on 30.03.2020:

Our gross loan portfolio is EUR 39 million and provides the Group companies with stable and sufficient operating cash flows to manage the existing portfolio, debt and run daily operations without interruption. Meanwhile, on a preventive basis, we are taking all necessary actions to manage our cost base with maximum efficiency. We are fully prepared for turbulence in case it comes to Botswana, Namibia or Zambia.

If the same Finko script is used, then I expect following to happen:

Mogo will acquire Expresscredit Botswana or Expresscredit Namibia, or both.

Expresscredit Zambia will go into wind-down

Expresscredit Group will be removed from Mintos as a Loan Originator

For Expresscredit Botswana and/or Namibia investors this will be a good thing, for Expresscredit Zambia investors - well, good luck holding your bag, wait till 2022 or whatever estimate is later published to find out, if you will get anything back.

Latest update from Mintos about situation is Namibia does not look promising:

The moratorium for borrowers in Namibia became effective on 26 March 2020. The credit holidays are valid for both principal and interest payments and can be in power for a period from 6 to 24 months. During the grace period, if a reduced interest rate would be applied, interest might be capitalized.

AS "Zen Group"

Just like in examples already mentioned, we see the same 3 persons from Mogo: CFO, CEO and Group Chief Risk Officer.

What about other 2 guys? They are both members of the board at Zenka Group, which is described in following way:

Zenka Finance is a fintech company set up in December 2018 to provide innovative personal flexible loan products. The typical clients of Zenka are men – educated, aged 25-45, running their own business or employed in the public/private sectors and living in the Nairobi region in Kenya.

Some of the equity investors in the loan originator and Mintos overlap.

And the only beneficial owner of AS Zen Group is Aigars:

What about Zenka Group? Any signs of trouble? It is rated quite low: C+, but otherwise seems to be fine - no pending payments, not suspended.

Of course, some investors might want to reconsider investing in Kenya after seeing issues with Zambia, but overall the feeling is that in this case Zenka Group might be added to Mogo not because it has become “toxic“, but with goal to simplify things and build up Mogo as the next 4Finance to be sold or IPOed.

And if Zenka gets assigned Mogo’s A rating after adding it, then of course - it will get easier to get Mintos investor money for loans in Kenya. I guess the interesting question is: will Mogo remove their group level guarantee after adding risky loan originators to their portfolio? If not, what will happen in the next Varks/Monego case? Will then the toxic companies be sold and removed from Mogo group?

AS "NF Capital"

Just like in other cases, we see the same 3 persons from Mogo: CFO, CEO and Group Chief Risk Officer:

And again, Aigars as the only beneficial owner:

What about other 3 guys? They are all from Finitera. Depending on who you ask, there might be 2 different answers about which companies are included in Finitera:

Martins, CEO of Mintos, confirmed in interview - that Monego is part of Finitera, and if it was not, then why did Finitera promise to buy back it’s late loans?

On Mintos Loan Originator page only Kredo and Tigo are listed under Finitera

What about potential deal between Mogo and Finitera? I think it is very likely that we will see the same Finko script here:

Mogo will acquire Finitera (only the “good parts“: Kredo and Tigo)

Monego has already gone into the process of liquidation

Finitera, Monego will be removed from Mintos

What does it mean for Mintos investors?

If at first there was an expectation and feeling that the 4 biggest Mintos shareholders would do anything possible to avoid losses for investors, then right now based on their actions and possible future events it looks to me that their stategy has changed:

If you invested in any of problematic loan originators, even if they were connected to one or more of 4 Mintos investors, don't expect too much. You probably made a mistake and maybe you will get something back, maybe not. These companies have become toxic, most likely won't get further funding and will be shut down.

The Mogo life-boat has a limited size, so the best loan originators that have not run into issues yet, might be acquired by Mogo. And there are several benefits:

Mogo will get bigger, expand to more markets and segments

Mogo has more diverse funding sources: bonds + Mintos

Mogo has the best rating on Mintos, and that will probably be assigned to all the loan originators that it acquires

Same shareholders, so what?

I think the key thing in all of this is how the these 4 shareholders look at Mintos investors?

a) are Mintos investors seen as dumb money and potential bag holders when things go wrong?

b) are Mintos investors seen as an important funding source that you don't want to mess with?

Let’s check which problematic loan originators are connected to the same 4 Mintos & Mogo shareholders:

If all of these companies were part of Mogo from Day 1, would they still act in the same manner - aggressive growth, losing licenses, and many wind-downs? Not sure.

But now - good assets are moved to Mogo, and Mintos investors can hold the bags with 46 million EUR at risk from failed Loan Originators.

Update @ 22.09.2020

The publishing of this post was delayed for a week because I agreed to Mogo’s request. Seems like the reason for delay was because at least 1 of my predictions was correct:

22.09.2020 @ Mintos blog: Mogo Finance plans to acquire Tigo and Kredo

Will other deals happen? No idea, let’s wait and see.

Update @ 23.09.2020

I updated the “at risk” table - previously I made calculations based on outstanding+pending+in recovery stats, but changed it by taking data from Mintos PDF reports, and also included calculations about recovered amounts so far.

And another reminder about my own potential conflicts of interest:

My wife works at Mogo, which is one of the biggest loan originators on Mintos

MaxTraffic, where I am the biggest shareholder, has clients from lending sector

P.S. Join “High-risk investments“ Telegram group for an informal discussion.

Awesome investigation. Thank you so much! I guess, many Lithuanians will be reading it after I posted link in our P2P group in Facebook. You should receive an award from Latvian government (looks like your are from LV).

Thank you for your research. At first I thought that the originators would act in our best interests but this was naive of me. Now COVID has them leaving us with the bag and they are being as sneaky about it as possible. Guessing this is to keep Mintos investors in the dark as far as possible to keep our money in their system.

The diversification of originators is clearly just smoke and mirrors. Thank you again for this research, I'm getting out of this mirage ASAP.